AML Edtech · Netizen9

Greensill Capital / Credit Suisse — The $10 Billion Compliance Collapse

Source: NotebookLM · Netizen9 AML Edtech · amledtech.uk

Credit Suisse channelled over $10 billion of its wealthiest clients' money into funds run by Greensill Capital. The bank performed no independent credit assessment, ignored repeated warnings from 2017 onwards, and allowed Greensill to select its own assets and arrange its own insurance. When the insurer withdrew in March 2021, the entire structure collapsed in days.

Australian financier, founder of Greensill Capital. Operated largely unchecked inside Credit Suisse's asset management division. Charming, well-connected, the ultimate salesman.

Marketed four supply chain finance funds to wealthy clients as flexible, low-risk. Performed no independent credit assessment. Sales staff earned "shadow revenues" for promoting them.

Steel tycoon whose group defaulted on $5 billion. Allegedly funded by fictitious future invoices. The biggest single concentration failure in the collapse.

Former UK Prime Minister. Employed by Greensill post-government; lobbied ministers by text to gain access to COVID loan schemes. Biggest UK political scandal of the era.

Invested $1.5B+ in the Credit Suisse/Greensill funds at Greensill's personal request. Greensill then financed SoftBank portfolio companies — a circular flow of funding.

Refused to renew the insurance backing the investment products, concluding it could not assess the credit risk. Withdrawal of cover caused immediate collapse of the entire structure.

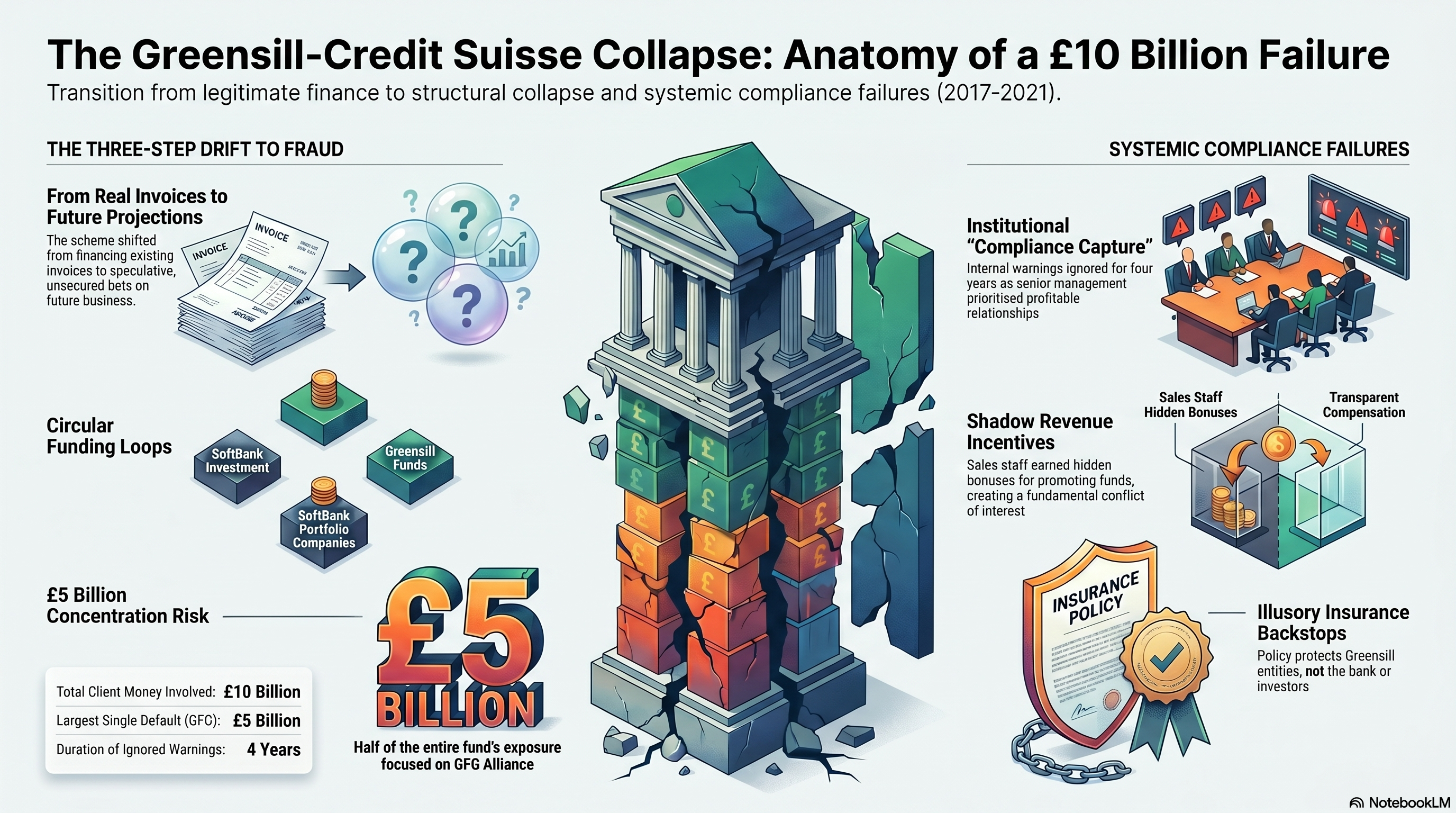

Supply chain finance is a legitimate instrument. The concept: a supplier raises an invoice, a finance provider pays immediately at a small discount, and waits for the buyer to settle. The risk is credit risk on a real, existing transaction. Greensill drifted from this in three steps — each one invisible to the investors whose money was at stake.

At its origin, Greensill financed real invoices between genuine trading counterparties. Credit risk was tied to identifiable buyers. The short-duration, self-liquidating nature of real trade finance made it genuinely low-risk. This is the product Credit Suisse described to clients.

Over time, Greensill began funding future receivables — claims that had not yet arisen — and eventually expectations of possible future business based on historical trading patterns. When you finance a real invoice, the underlying transaction has already occurred. When you finance a projection, you are making a speculative unsecured bet with a trade finance label. The product's risk profile had transformed; the disclosures to investors had not.

The structure became self-referential. SoftBank invested $1.5 billion into the Credit Suisse/Greensill funds. Greensill used those funds to finance SoftBank portfolio companies. Those companies generated the "receivables" that backed the fund assets. The money was going in a loop — each leg appearing legitimate in isolation while the circle as a whole had no external anchor.

Simultaneously, GFG Alliance — Sanjeev Gupta's empire — had grown to represent approximately $5 billion of the total book. A single counterparty group had become the dominant exposure. When GFG defaulted, there was no diversification to absorb it.

The products were marketed with an insurance backstop. Investors and apparently the bank's own risk team believed this protected fund assets. In reality, the insurance policy paid out not to Credit Suisse or to fund investors — but to Greensill's own entities. When Tokio Marine refused renewal, the entire structure collapsed because the protection investors believed they had never existed in the form described.

Internal advisors earned "shadow revenues" for promoting the Greensill funds. Independent advisors without these bonuses rarely recommended them. This is a structural conflict — not a rogue adviser problem.

Any remuneration structure that creates an incentive to sell a specific product regardless of suitability is a fundamental compliance failure. Conflicts must be identified, managed and disclosed; where they cannot be managed, the business must be declined.

In 2017, Greensill completed a self-filled questionnaire. FINMA later described it as wholly inadequate and found that clear contradictions and red flags were never scrutinised. For a $10 billion product line, the minimum standard for counterparty onboarding was not even approached.

Self-certification is not due diligence. Proprietary questionnaires must be verified against audited accounts, regulatory filings, news searches and legal records. The person completing the form always has an incentive to present their business favourably.

Rather than classifying funds as "new business" — which would trigger rigorous governance review — they were labelled "new products," skirting stricter oversight. This was active circumvention, not passive failure. Someone made a deliberate decision to avoid the harder scrutiny path.

Compliance must own classification decisions — not accept the classification proposed by those with a financial interest in a lighter-touch outcome. Where a business originator consistently categorises transactions in the lowest-scrutiny category, that pattern is itself a red flag.

Credit Suisse did not conduct independent credit assessment of the receivables in the funds. It left that to Greensill — who had a direct financial interest in every deal proceeding. Credit Suisse also left Greensill to arrange insurance cover in Greensill's own name.

Independence in credit assessment is not optional. Delegating the selection or valuation of assets to the originator — who profits from every deal — is a complete abdication of fiduciary duty. FINMA treated this as a serious regulatory violation.

Greensill funded claims that had not yet arisen and projections of possible future business. The products continued to be marketed as low-risk, short-duration trade finance. The actual risk profile was never disclosed to investors.

Product labelling must reflect actual risk. Where underlying assets drift from the original profile, investors must be informed. Continuing to market a product as low-risk when the assets have become speculative is both a mis-selling failure and a prospectus violation.

GFG Alliance defaulted on approximately $5 billion — a single counterparty group representing the dominant exposure in the entire book. Either concentration limits didn't exist, were set indefensibly high, or were overridden.

Single-name concentration limits are structural controls, not aspirational guidelines. They must be set at the portfolio level and enforced independently of originator pressure. One borrower's default should never be able to destroy a fund.

SoftBank invested into the funds. Greensill financed SoftBank companies. Those companies generated the receivables backing the fund assets. The money circulated. A proper network analysis of counterparty relationships would have identified this immediately.

Circular or self-referential funding structures are a fundamental red flag in AML and credit risk frameworks. Where the same capital appears in multiple legs of a transaction chain, apparent diversification is illusory. Network mapping is essential for any complex structured product.

Concerns were communicated to senior Credit Suisse managers from 2018 onwards. Anonymous internal messages challenged leadership's judgement. FINMA found evidence of this pattern. The problem was not that warnings were never raised — it is that they went nowhere.

A compliance function that can identify problems but cannot stop business is a legal shield, not a control. The test of compliance culture is whether concerns are acted upon when doing so costs the bank money. Where senior management can override compliance, the organisation will eventually pay the price.

Product board meetings proceeded with critical absences — including top executives responsible for the funds — raising doubts about the integrity of the approval process itself.

Governance that proceeds without key decision-makers, relies on incomplete information, or is driven by those with financial interests in the outcome is documentation, not oversight. Accountability must attach to individuals, not committees.

The insurance paid out not to Credit Suisse or fund investors but to Greensill's own entities. The risk transfer the entire structure was supposedly built on did not exist in the form described to investors.

Where a product's risk profile depends on a credit enhancement or backstop, verify: who is the beneficiary? What triggers payment? Is the insurer actually exposed to the risk described? "Insurance exists" is not sufficient — the terms must be independently verified.

The compliance structures existed. The governance processes existed. The warning mechanisms existed. None had authority when they came up against a profitable relationship senior people wanted to protect. The compliance function had been captured by the business it was supposed to police. This is the most dangerous kind of compliance failure — not ignorance, but capture.

Your firm provides trade finance. A long-standing client asks you to finance not just existing invoices but "expected future orders" based on historical trading patterns. The return is higher. What is your compliance response?

Future receivables are not trade finance — they are speculative unsecured lending with a trade finance label. Require re-classification, revised pricing and full disclosure. If the client refuses, decline.

A senior salesperson's bonus is tied directly to volume of one specific fund product. Two junior advisers tell you they felt pressured to recommend it despite reservations. What do you do?

This is a structural conflict under FCA SYSC and MiFID II inducement rules. Escalate immediately. All clients sold the product require an independent suitability review. The bonus arrangement must be redesigned.

During EDD on a fund, you identify that its largest investor is also the parent of several of the fund's major borrowers. The manager calls it "strategic alignment." What concerns does this raise?

Circular funding creates systemic risk and masks the true risk profile. Require full transparency on all counterparty relationships, network mapping and independent stress testing before proceeding.

A compliance officer documented concentration risk concerns 18 months ago. The concern was escalated and overridden by the head of business with CRO approval. The counterparty has now defaulted. As MLRO, what is your assessment?

An override does not extinguish compliance responsibility — it increases it. Assess whether a SAR obligation arose at the time of the override or subsequently. Document the full timeline, seek legal advice and report the culture failure to the board.

Reading an insurance policy schedule carefully for the first time, you realise it pays out to the originator's holding company — not to the fund or its investors, as described in the information memorandum. What do you do?

This is a material misrepresentation to investors. Halt further distribution immediately. Notify the board, the FCA and legal counsel. A client notification and potential product recall may be required. Assess SAR obligation in respect of the mis-selling itself.

| Provision | Relevance to This Case |

|---|---|

| FINMA Enforcement | Found Credit Suisse committed serious regulatory violations — inadequate due diligence, failure to act on warnings, failure to manage conflicts of interest. Structural remedies imposed. |

| FCA COLL Sourcebook | Fund management rules: counterparty concentration limits, risk management obligations, requirement for independent credit assessment, investor disclosure requirements. |

| FCA SYSC | Systems and controls: conflicts of interest identification, management and disclosure; internal governance and accountability structures; remuneration arrangements. |

| MiFID II — Product Governance | Manufacturer and distributor obligations to ensure products are suitable for their target market; prohibition on inducements that create conflicts with client interests. |

| MiFID II — Conflicts of Interest | Inducement rules: shadow revenues paid to internal advisers to promote specific products are inducements that must be disclosed or prohibited. |

| FSMA 2000 s.89–91 | Market abuse and misleading statements — continued marketing of products as low-risk when underlying assets had become speculative in nature. |

| POCA 2002 | Where fictitious invoices were used as fund assets, potential proceeds of fraud. SAR obligations for regulated firms processing transactions connected to the funds post-collapse. |

| FCA Conduct of Business (COBS) | Suitability obligations: products must be suitable for the clients they are sold to. Wealthy clients are not automatically sophisticated investors for all purposes. |

| Companies Act 2006 | Directors' duties — relevant to Greensill's own board governance failures and potential liability for those who signed off on the structure. |

The employment of David Cameron and his subsequent lobbying of ministers by personal text message — seeking access to COVID-19 emergency lending schemes for Greensill — triggered the UK's most significant political sleaze scandal in years. A parliamentary inquiry was held. An independent review led by Nigel Boardman examined the relationship between Greensill and government. The episode illustrated a systemic problem: the revolving door between senior government roles and finance, and the access it buys.

For compliance professionals: the political connection was itself a red flag. A company whose business model depended on government access, and which employed former heads of government to lobby on its behalf, was structurally dependent on political relationships for commercial survival. That dependency is a material risk that should have appeared in any serious due diligence.