AML Edtech · Netizen9

Trafigura v Gupta — $600 Million Nickel Fraud Case Study

Source: NotebookLM · Netizen9 AML Edtech · amledtech.uk

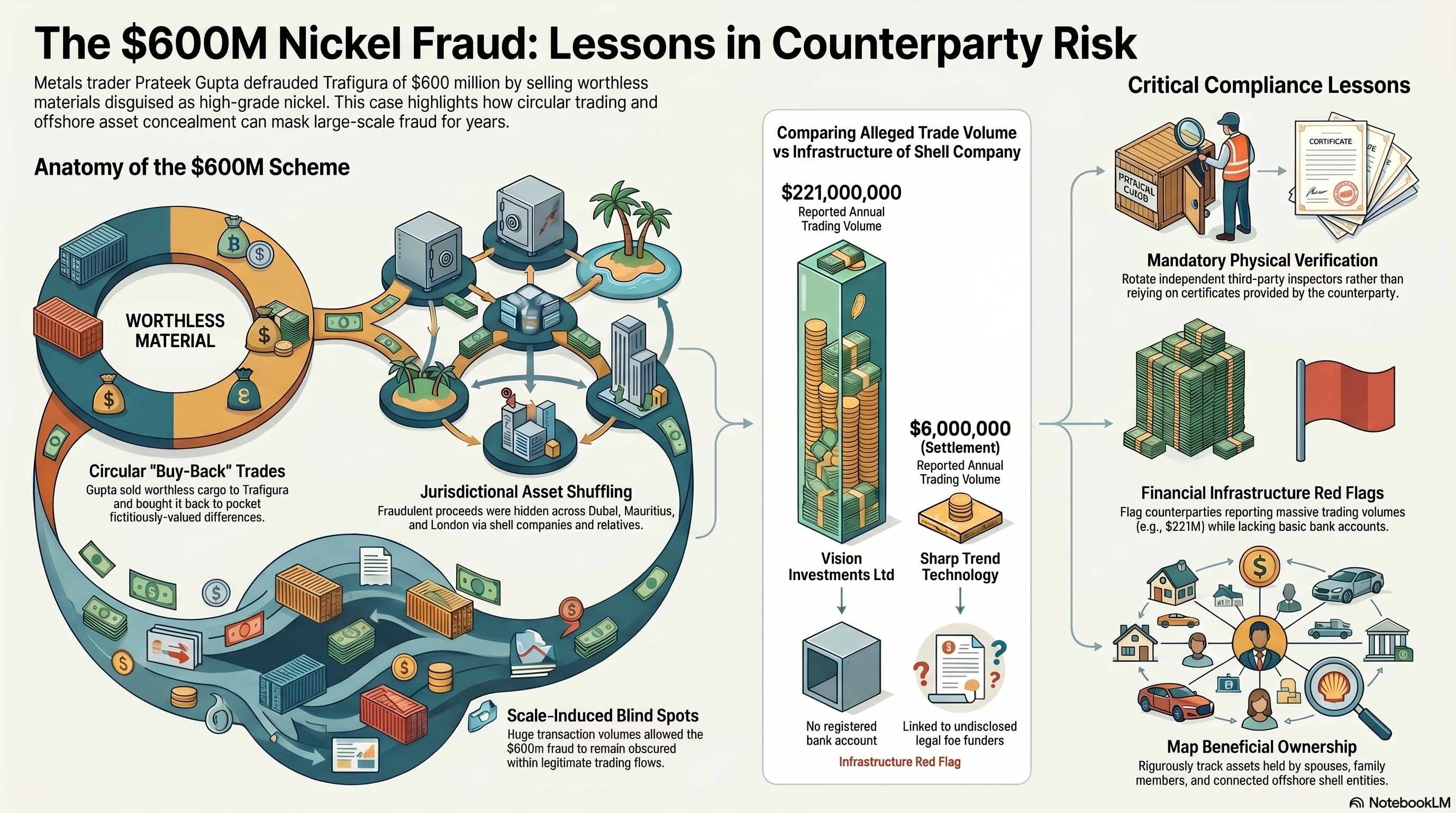

In 2026, Trafigura — one of the world's largest commodity trading companies — obtained judgment against metals trader Prateek Gupta in the English courts. The fraud: $600 million in worthless nickel cargoes sold as premium material over years of trading. With interest, total damages exceed $700 million.

The fraud was built around buy-back sales of nickel cargoes. Gupta sold cargoes described and certified as premium high-grade nickel to Trafigura. In reality, the cargoes were largely worthless substitute material. Gupta then bought back the cargoes, completing a circular structure that gave the appearance of legitimate two-way trading. He pocketed the difference between what Trafigura paid and the actual value of what was delivered.

The cycle repeated over years. Each transaction appeared superficially routine. The fraud did not involve a single spectacular theft — it accumulated through small, repeated normalisations, each individual trade acceptable enough not to trigger alarm.

Buy-back structures mimic legitimate trading. In commodity markets, round-trip transactions occur for genuine commercial reasons — hedging, position management, inventory rebalancing. The fraud was camouflaged within normal market activity.

Physical inspection is complex at scale. Nickel is a bulk commodity stored in warehouses, ships and port facilities across multiple countries. Confirming grade and composition requires independent verification — which was absent.

Relationships create trust. Long-running trading relationships generate track records. Each apparently successful cycle reinforced the apparent legitimacy of the next. At Trafigura's transaction volumes, a $600 million fraud accumulated over years could be obscured within aggregate flow.

The fraud generated very large proceeds. Evidence before the courts suggests these were concealed through a layered structure designed to insulate assets from future creditors across multiple jurisdictions.

Substantial assets were placed in the name of Ginni Gupta. Trafigura alleged that the "natural inference" is that fraudulent proceeds were carefully placed in his wife's name to insulate them from creditors — a classic asset protection technique creating legal distance between the fraudster and the assets.

Vision Investments Limited, a company in which Mrs. Gupta holds shares, reported metals trading volumes of $145 million in 2018 and $221 million in 2019 — yet reportedly had no bank account. A company trading at this scale with no visible banking infrastructure raises fundamental questions about where the money actually went.

Mrs. Gupta acquired assets worth tens of millions, including an indirect stake in Mauritius' Silver Bank. Cross-border placement — particularly into offshore financial centres — is a well-established technique for making assets harder to trace and seize.

A company allegedly associated with a member of the Abu Dhabi royal family funded both Guptas' legal fees. Trafigura's barrister told the court: "It looks thoroughly uncommercial." A funder with no financial interest in the outcome, funding both defendants — this is a significant red flag that hidden arrangements exist.

After the London judgment, Mrs. Gupta sold a Dubai villa as part of a $6 million settlement. The funds were sent to a company alleged to be associated with the same litigation funder. This illustrates a common pattern in post-judgment asset concealment: moving assets through a chain of apparently unrelated transactions to obscure the final destination of funds.

Worthless material passed as high-grade nickel because counterparty-provided certificates were treated as sufficient. They are not. Independent third-party inspection at loading and discharge is essential. The inspector must be appointed by the buyer, not the seller.

Any transaction where you are both selling to and buying from the same counterparty in a repeating pattern is a structural red flag. Buy-back transactions require senior sign-off and specific documentation of commercial rationale. Profitability is not a reason to relax scrutiny — it may be a reason to increase it.

$221 million in trading revenue with no bank account. This inconsistency, identified at onboarding or periodic review, should have terminated the relationship. Financial infrastructure must be proportionate to claimed activity.

Assets were placed in a spouse's name specifically to create legal distance. Standard KYC on the direct counterparty would not have surfaced these holdings. Beneficial ownership mapping must extend to spouses, family members and closely connected entities.

Long-running frauds persist because trust accumulates. Each successful transaction confirms the relationship. Periodic re-underwriting of significant counterparty relationships is essential — a deliberate reset, applying fresh eyes to the full profile as if onboarding for the first time. The longer and larger the relationship, the more important this is.

Assets spanned the UK, Dubai, Mauritius and Abu Dhabi. No single jurisdiction had visibility across the full picture. Geographic dispersal was structural — designed to prevent any one institution or regulator from seeing the whole. Where evidence of source of wealth cannot be obtained, the relationship should be reconsidered.

A transaction or arrangement that makes no commercial sense is a red flag that it is serving a different purpose. Third parties paying legal fees, providing credit or making gifts without obvious consideration are potential indicators that hidden arrangements exist. This applies in transaction monitoring as much as it does in court proceedings.

A counterparty with $200 million in assets held in New York, London and Singapore is a materially different recovery risk from one with the same nominal value in Dubai, Mauritius and Abu Dhabi held through layers of corporate structure. Asset location must be part of counterparty risk assessment — not just net worth.

A commodity trading firm has a three-year buy-back arrangement with a metals supplier. The supplier provides all quality certificates. Your transaction monitoring team flags that the same counterparty appears on both sides of every transaction. The trading desk says this is normal hedging. What is your compliance response?

Buy-back structure plus counterparty-provided documentation without independent verification are both red flags. Require independent physical inspection, commercial rationale documentation, senior sign-off and a retrospective review of prior transactions.

During EDD on a new corporate counterparty, you discover the company reports $145 million in trading revenue but its accounts reference no bank account. The representative says the company uses an intermediary settlement agent. What do you do?

Trading volumes inconsistent with banking infrastructure is a fundamental red flag. The relationship should not proceed without full and verifiable explanation of settlement mechanics, identification of the agent and source of funds verification.

Your counterparty is a successful commodity trader. Periodic review identifies that his wife's company has acquired assets worth $40 million over 18 months, including a stake in a Mauritius bank. Her stated source of wealth is family gifts. What are your obligations?

Connected party enrichment is a material red flag for proceeds placement. Source-of-wealth claims must be evidenced. Notify the MLRO. A SAR may be required depending on the totality of the information.

Your client's account receives a $3 million transfer from a company described as a "litigation support provider." Your client is the defendant in a large commercial fraud case. The payer would receive no financial benefit even if your client wins. What is your assessment?

A commercially irrational payment is a red flag under every AML framework. The absence of benefit to the payer suggests the payment serves an undisclosed purpose. This warrants a SAR assessment and potentially a DAML consideration if further funds are expected.

You are processing a payment from your client. She has sold a Dubai property for $6 million. The proceeds are being paid to a company described as a debt collection agency. You are aware your client is subject to a freezing order in a foreign jurisdiction. What do you do?

Assisting in the transfer of assets subject to a foreign freezing order may constitute a prohibited act. Obtain legal advice immediately. Processing without DAML may expose the firm to POCA liability. This also triggers a SAR obligation.

| Provision | Relevance to This Case |

|---|---|

| POCA 2002 s.327 | Concealing, disguising, converting or transferring criminal property — the villa sale and cross-border asset movements |

| POCA 2002 s.328 | Arrangements facilitating acquisition, retention, use or control of criminal property — litigation funding and intermediary structures |

| POCA 2002 s.330 | Failure to disclose knowledge or suspicion of money laundering — applicable to any regulated firm processing transactions for connected entities |

| POCA 2002 s.333A | Tipping off in the regulated sector — banks must not alert the client that a SAR has been filed or that transactions are under review |

| POCA 2002 s.338 | Defence Against Money Laundering — DAML required before processing transactions where funds may be proceeds of crime |

| MLR 2017 Reg. 28 | Customer due diligence — connected party mapping, beneficial ownership, source of wealth |

| MLR 2017 Reg. 33 | Enhanced due diligence for high-risk situations — cross-border structures, offshore jurisdictions, PEP-connected entities |

| FATF Rec. 10 | Customer due diligence — the standard against which KYC failures in this case are measured |

| FATF Rec. 24 | Transparency and beneficial ownership of legal persons — Vision Investments and connected structures |

| ECCTA 2023 s.199 | Failure to Prevent Fraud — directly relevant where a firm's systems failed to detect or prevent the fraudulent scheme |

Winning in court is not the same as recovering money. The English judgment established fraud at over $700 million — but the assets are in Dubai, Mauritius and Abu Dhabi. Trafigura must pursue parallel proceedings in each jurisdiction, each with different procedural rules, timelines and enforcement standards. The UAE has two parallel court systems. An English judgment does not automatically transfer.

The time asymmetry problem: Moving money takes days. Litigating across jurisdictions takes years. The legal system in cross-border fraud cases structurally favours the person hiding assets over the creditor trying to recover them.